Loan allocation is one of the trickiest puzzles financial institutions face today. The old ways, relying on rigid credit scores and siloed processes, just don’t cut it anymore. When lending decisions move too slowly or miss crucial signals, the impact is real: missed chances, frustrated customers, and uneven risk exposure. It’s clear that the old playbook needs an upgrade.

Looking ahead, the market for AI agents in financial services is set to grow to nearly $8.95 billion by 2032. That’s not just a number; it’s a sign that more organizations are putting their faith in AI systems that keep an eye on the data 24/7 and adjust decisions as conditions change, whether it’s dynamically qualifying prospects, customizing financial products, or optimizing resource allocation in real time. It’s the kind of adaptability traditional models can’t match.

In this blog, we’ll unpack what AI agents for loan allocation in financial institutions actually bring to the table.

Takeaways

- Lending Challenges: Traditional models rely on static risk assessments, manual-heavy processes, and limited reach to underserved borrowers. Institutions also face regulatory hurdles, legacy systems, data quality issues, and transparency concerns, delaying effective AI adoption.

- Impact of AI: AI delivers real-time, adaptive decisions using diverse data, including alternative sources, to expand fair credit access. It also automates verification, fraud detection, and risk monitoring, cutting errors and costs while preserving human oversight where needed.

- Nurix Advantage: Nurix AI offers practical, end-to-end solutions across the loan lifecycle, combining automation with human input. By embedding actionable insights into workflows, we enable faster approvals, stronger risk management, broader market reach, and compliance-driven lending.

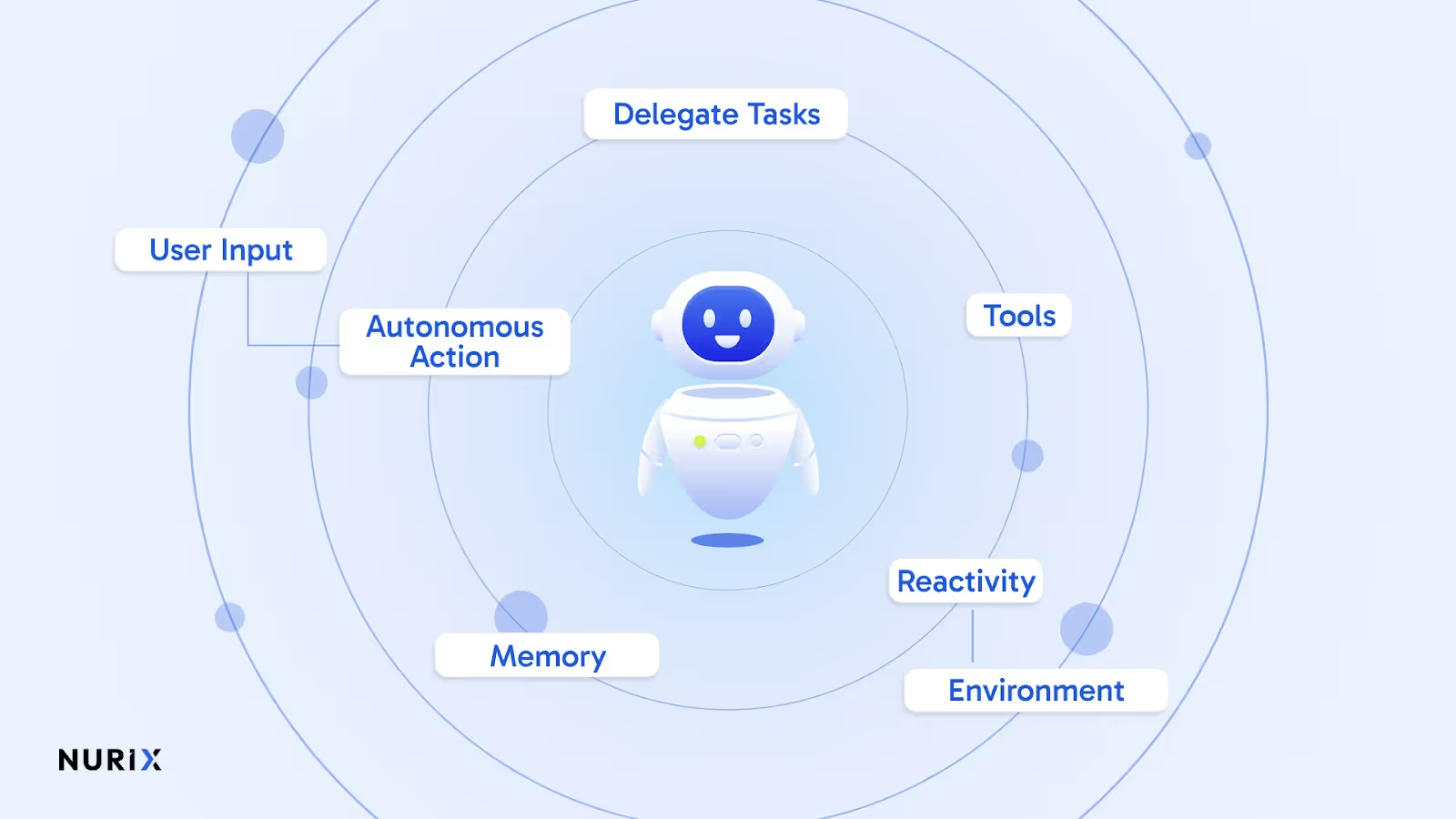

What Are AI Agents?

AI agents are autonomous software systems designed to execute tasks and make decisions independently, often operating with minimal human intervention. They combine advanced algorithms, machine learning models, and contextual data analysis to perceive their environment, reason through complex problems, and act purposefully to achieve specific objectives.

Having outlined what defines AI agents, the next layer is why financial institutions turn to AI agents for loan allocation in financial institutions to handle specific challenges in lending decisions.

Why are Financial Institutions Looking for AI Agents?

Traditional loan allocation exposes several persistent weaknesses that limit speed, accuracy, and fairness in lending decisions. These pressure points highlight why financial institutions are increasingly considering AI agents as a way to improve loan workflows and outcomes.

- Manual and Fragmented Processes: Traditional loan allocation typically involves multiple manual steps across different departments, resulting in a slower, error-prone process that often lacks end-to-end visibility.

- Inadequate Risk Assessment: Legacy systems rely on static credit scoring models that inadequately capture nuanced borrower risk factors, leading to higher default rates or overly conservative lending.

- Inefficient Resource Deployment: Banks often allocate excessive resources towards screening or marketing efforts rather than balancing these activities, causing misaligned priorities between attracting borrowers and evaluating creditworthiness.

- Limited Real-Time Adaptation: Traditional loan allocation systems fail to dynamically adjust to market changes or borrower behavior, which increases exposure to risk and missed lending opportunities.

- Bias and Lack of Granularity: Manual underwriting decisions may introduce unconscious bias and lack the granular data interpretation necessary to differentiate between high- and low-risk applicants accurately.

- Inflexibility in Portfolio Management: Existing models struggle to optimize loan portfolios holistically, making it difficult to balance profitability against risk dynamically.

Here’s an interesting read: AI Chatbots for Banking and Finance Management

Full-Stack Loan Allocation Agent Blueprint

Breaking down the core modules that come together to automate lending decisions and manage risk with precision and adaptability.

- Perception Layer: Continuously gathers multi-dimensional borrower data, including credit history, transaction patterns, and non-traditional indicators like social behavior or cash flow analytics.

- Decision-Making Core: Applies advanced machine learning algorithms trained on historical and real-time data to evaluate borrower risk, predict default probabilities, and recommend loan terms precisely matching risk profiles.

- Resource Allocation Module: Balances screening and marketing efforts by dynamically adjusting resource investment based on demand trends, borrower quality, and regulatory constraints.

- Risk Management Engine: Monitors portfolios continuously to identify emerging risks, reallocates loan capital proactively, and enforces compliance with risk appetite frameworks.

- Learning System: Incorporates feedback loops from loan performance data and external market signals to refine credit scoring models and decision thresholds over time.

- Action Interface: Automates execution of loan approvals, rejections, or escalations with configurable parameters for human oversight when necessary, enabling faster processing and reducing operational costs.

- Reporting and Transparency Dashboard: Provides real-time insights into loan pipeline status, risk distribution, and allocation fairness to support auditability and regulatory compliance.

With the challenges clear, it’s worth examining how AI agents for loan allocation in financial institutions are actively reshaping key aspects of lending, moving beyond theory into practical impact.

You might want to read this: Use Cases and Role of Large Language Models in Finance and Banking Industry

Top Ways AI Agents Are Transforming Loan Allocation in Financial Institutions

Loan allocation is complex, and AI agents aren’t just automating tasks; they’re changing how key decisions get made. Below are concrete ways these systems tackle persistent challenges and bring new capabilities into the lending process.

1. Intelligent Risk Assessment and Predictive Analytics

AI agents transform credit risk evaluation by analyzing complex patterns across multiple data sources to predict loan performance before traditional metrics would reveal potential issues. Neural network models achieve 91% accuracy in loan default prediction, significantly outperforming conventional scoring methods.

Key Use Case Details:

- Advanced Behavioral Analysis: AI systems monitor borrowers' financial behavior in real-time, analyzing transaction patterns, cash flow volatility, and spending habits to identify early warning signals that indicate potential financial distress.

- Multi-Source Data Integration: Agents combine traditional credit data with alternative sources, including utility payments, employment history, and digital footprints, to create comprehensive risk profiles, expanding credit access by 27% for previously underserved segments.

- Dynamic Risk Scoring: Machine learning models continuously update risk assessments based on changing economic conditions and borrower circumstances, enabling more accurate pricing and proactive interventions.

2. Automated Document Processing and Verification

AI agents streamline loan origination by automatically extracting, verifying, and validating information from complex financial documents, reducing processing time from days to minutes while maintaining 99% accuracy rates.

Key Use Case Details:

- Intelligent OCR Technology: Advanced optical character recognition combined with natural language processing extracts data from varied document formats, including scanned copies, photos, and handwritten forms, eliminating manual data entry errors.

- Fraud Detection Capabilities: AI systems identify document tampering and suspicious activities by analyzing metadata, formatting inconsistencies, and cross-referencing information against databases, preventing 5% of loan applications containing falsified documents.

- First Notice of Loss (FNOL) Integration: For lenders offering insurance-linked products, AI agents digitize and streamline the filing of FNOL during loss events such as accidents or asset damage. Customers can submit claims instantly via mobile apps or chat interfaces, while the system verifies supporting documents, cross-references claim details, and initiates downstream processing.

- Real-Time Authentication: Agents verify document authenticity through integration with government databases and third-party verification services, ensuring compliance while accelerating approval workflows.

3. Personalized Customer Engagement and Support

AI-powered conversational agents provide 24/7 customer support throughout the loan lifecycle, handling routine inquiries while delivering personalized guidance based on individual borrower profiles and preferences.

Key Use Case Details:

- Multi-Channel, Multilingual Engagement: Customers can interact through websites, mobile apps, WhatsApp, or voice channels, with the experience tailored to their preferred language and communication style. Context is preserved across channels, ensuring smooth, uninterrupted support.

- Tiered Query Support (L1 & L2): Routine borrower queries, such as loan details or repayment schedules, are instantly resolved (L1), while more complex questions, like repayment simulations or risk-based clarifications, are handled intelligently at an L2 level. Complex cases escalate smoothly to human agents with full context transfer for faster resolution.

- Risk-Aware Interaction: AI integrates real-time risk insights into conversations. Early warning signals such as missed payments or irregular activity trigger proactive nudges, flexible repayment options, or escalation to risk teams, balancing customer care with portfolio protection.

- Proactive Payment Management: Personalized reminders are sent ahead of due dates through preferred customer channels, with contextual prompts like autopay setup or alternative plans for at-risk borrowers. This ensures repayment discipline while easing customer stress.

- Intelligent Application Guidance: Borrowers receive step-by-step guidance during the application, with real-time eligibility checks and document validation. This not only reduces abandonment but also builds trust through clear, transparent communication.

4. Real-Time Portfolio Monitoring and Optimization

AI agents continuously monitor loan portfolios to identify performance trends, predict defaults, and recommend strategic adjustments to maximize returns while minimizing risks across the entire loan book.

Key Use Case Details:

- Early Warning Systems: Machine learning models detect subtle changes in borrower behavior, economic indicators, and market conditions to flag at-risk loans before delinquency occurs, enabling timely interventions.

- Automated Portfolio Segmentation: AI categorizes loans by risk level, profitability, and repayment behavior to support targeted strategies for different borrower segments and optimize capital allocation.

- Performance Analytics: Advanced algorithms analyze historical data and current trends to provide actionable insights for loan pricing, retention strategies, and risk mitigation, improving portfolio profitability significantly.

5. Automated Collections and Recovery Management

AI agents transform debt collection by implementing empathetic, data-driven communication strategies that improve recovery rates while maintaining positive customer relationships throughout the collections process.

Key Use Case Details:

- Smart Communication Optimization: AI analyzes customer interaction history to determine optimal contact timing, channel preferences, and message content, increasing engagement rates and payment compliance.

- Personalized Recovery Strategies: Machine learning models assess individual borrower circumstances to recommend appropriate collection approaches, from gentle reminders to structured payment plans based on financial capacity.

- Compliance Automation: AI ensures adherence to regulatory requirements by maintaining detailed audit trails, monitoring communication frequency, and automatically escalating accounts according to legal guidelines.

6. Alternative Data Integration for Credit Scoring

AI agents expand financial inclusion by incorporating non-traditional data sources into credit decisions, enabling institutions to serve previously unbanked populations while maintaining risk management standards.

Key Use Case Details:

- Digital Footprint Analysis: AI evaluates mobile phone usage patterns, social media activity, and online behavior to assess creditworthiness for borrowers with limited traditional credit history, improving approval rates for underserved segments.

- Transaction Pattern Recognition: Machine learning algorithms analyze utility payments, rental history, and recurring transactions to build comprehensive financial profiles that traditional scoring methods might miss.

- Behavioral Scoring Models: AI systems process psychometric data, employment stability, and lifestyle indicators to predict repayment likelihood, enabling more inclusive lending decisions while maintaining portfolio quality.

What Could Be Holding Financial Institutions Back From Implementing AI Agents?

The barriers to adopting AI agents for loan allocation extend beyond technology; they involve regulatory, organizational, and practical complexities that shape decision-making within financial institutions. Let’s break down where these challenges often arise.

- Regulatory Uncertainty and Compliance Challenges: Financial institutions face complex and evolving regulatory frameworks around AI use in lending. Unclear or shifting rules on data privacy, AI transparency, and credit decision fairness impede confidence and slow adoption. Continuous monitoring and cooperation with regulators are necessary to meet these obligations.

- Data Quality and Governance Issues: Poor data quality, fragmented legacy systems, and inconsistent data management undermine AI models’ accuracy. Banks struggle to create trustworthy, comprehensive datasets required for AI-driven credit risk evaluation. Establishing stringent data governance and cleaning protocols is critical but resource-intensive.

- Security and Privacy Concerns: The protection of sensitive financial and personal borrower data from cyber threats and unauthorized access is a top concern. AI systems must incorporate rigorous security measures, including encryption and access controls, which add technical complexity and cost.

- Talent Shortage in AI Skills: There is a notable scarcity of professionals skilled in AI design, development, and governance, specifically customized to financial lending needs. This talent gap limits the ability to build, validate, and manage AI agents effectively within financial institutions.

- Integration with Legacy Systems: Many financial organizations rely on outdated infrastructure that poses significant challenges for embedding AI agents in existing loan processing workflows. Integration struggles lead to delays, higher costs, and potential disruptions.

- Concerns Around AI Bias and Transparency: Without transparent and auditable AI models, there is a risk of biased loan decisions that may lead to regulatory repercussions and customer distrust. Developing explainable AI that meets ethical standards and complies with anti-discrimination regulations is challenging.

- Cost and Resource Investment: Developing, validating, and maintaining AI agents requires substantial upfront investment in technology, training, and continuous oversight. Financial institutions must balance these costs against uncertain near-term returns, limiting enthusiasm for broad deployment.

- Unclear AI Strategy and Risk Management Framework: Lack of a coherent AI adoption strategy aligned with institutional risk tolerance can hinder progress. This includes insufficient frameworks to assess AI model risk, biases, and operational impacts before and after deployment.

How Financial Institutions Can Improve Their Processes Using Nurix AI

Nurix AI accelerates sales, streamlines claims processing, and improves customer interactions through AI-powered automation that maintains a human touch where needed. It automates lead qualification, claim intimation, and policyholder support to enhance operational performance.

Key Features

- Automated Lead Qualification & Sales: AI agents analyze customer intent and qualify leads automatically, allowing sales teams to focus on high-potential prospects and increase conversions.

- First Notice of Loss (FNOL) Automation: Accelerates claims reporting with real-time updates and document handling, reducing delays and enhancing customer satisfaction.

- 24/7 Omnichannel Customer Support: Provides instant responses across voice, chat, and messaging, handling policy inquiries, renewals, and claims without increasing agent workload.

- Policy Renewal & Customer Retention: Proactively engages policyholders with renewal alerts, policy adjustments, and exclusive offers to reduce churn and improve profitability.

- Real-Time Agent Assistance: During live interactions, AI offers sentiment analysis, compliance checks, cross-sell prompts, and post-call quality assessment to boost performance and customer experience.

- Fraud Detection & Risk Management: Identifies suspicious activities early in the claims process to minimize losses and protect business integrity.

- Smooth System Integration: Works within existing CRM, policy administration, and claims systems for rapid deployment without overhauling infrastructure.

- Multilingual & Contextual Understanding: Supports native-language customer engagement, adapting to cultural communication nuances to increase market reach and satisfaction.

Conclusion

Loan allocation is evolving beyond simple number crunching and rigid checklists. AI agents for loan allocation in financial institutions offer a continuous pulse on borrower data and risk factors, moving lending decisions closer to real-time business realities. This shift challenges traditional mindsets about credit and risk, showing that adaptability and precision don’t have to be at odds.

For organizations ready to rethink loan workflows, Nurix AI provides a focused solution that doesn’t just automate steps but streamlines complex processes, from lead qualification through risk monitoring, while keeping human judgment in the loop where it counts. Get in touch with us!